-

August 2025 MyPlanIQ Portfolio Update

In this issue:

- Residential Real Estate vs. Stock Investments

- Fund Analysis: PIMCO Multisector Bond ETF PYLD

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

The Most Reliable Retirement Savings: Why $1.8 Million is a Popular Lie

In this issue:

- Latest in Retirement Savings & Personal Finance: Retirement Savings Still Fall Short, Sluggish Home Sales & The Most Overvalued Stock Market

- The Most Reliable Retirement Savings Needed: Why $1.8 Million is a Popular Lie

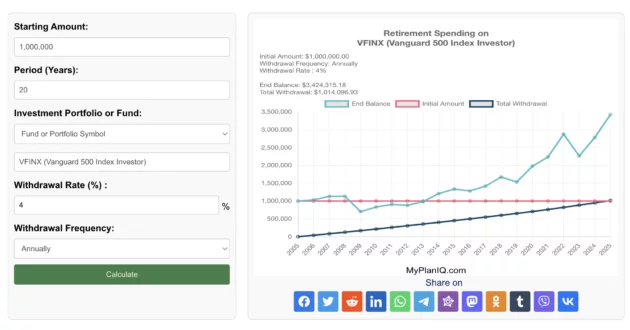

- Tools & Tips: Retirement Spending Calculator Based on a Portfolio, Fund, or Stock

- Market Overview

-

The Most Reliable Retirement Savings Amount You Need in 2025

You’ve probably come across those big retirement numbers that show up in media or surveys. Most of them sound a lot higher than what many people can actually save. Here are some popular ones: In this article, we will walk you through to show how an American with median income needs far less than the above headline numbers to retire at a similar quality life before retirement. A simple retirement spending formula is to utilize so called 4% wtihdrawal rule: the conventional wisdom goes that if you manage to withdraw 4% every year in a conservative investment portfolio (such as 70% in bonds and 30% in stocks), you probably will end up being able to extend your capital beyond 25 years: remember spending 4% every year in an account without much investment gain will deplete the account completely in 25 years (100%/4%=25). Financiall planners often use this 4% as a rule of thumb to gauge how much retirement income you need. Or put it another way, if you need to spend $10,000 a year, you would need to save $10,000 * 25 =$250,000 income before the retirement. So here are some numbers we can play with a typical American of 65 year old with median income: According to BLS data summarized by SmartAsset, full‑time workers aged 65+ earn a median of roughly $60,268 per year. Financial planners generally advise replacing 75%–85% of pre‑retirement income; Schwab specifically recommends about 80%. That puts your retirement income target at about $48,000 annually. Meanwhile, the average newly retired worker collects about $2,000 per month in Social Security, or $24,000 per year, as of 2025. That equates to Social Security covering nearly half your income goal, leaving a gap of $24,000 per year. Under the 4% safe withdrawal rule, you’d need only $24,000 * 25 = $600,000 (as 100%/4%=25) in savings to generate that supplemental income. This is far less than the headline figures! Why $600K Can Be Enough That’s not to say larger balances are useless. But if you can invest $600K conservatively and consistently earn about 4% after inflation, that portfolio should support a stable $24,000 annual withdrawal. It could last decade, and you can still manage to leave something over at the end. This amount also reduces pressure to chase high‑risk strategies during market fluctuations. In comparison, obsessing over a $1.8 million goal may mislead you into delaying retirement unnecessarily or taking undue risks. Why Realistic Targets Matter — Both Psychologically and Economically Setting an overly ambitious savings target like $1.8 million can create anxiety, discouragement, or inaction. Many people in their 50s or 60s with $300K–$400K saved may feel they’ve already failed, even if they are on track for a comfortable retirement based on income replacement. That psychological burden can erode confidence and planning energy. Economically, inflating your savings goal can steer you toward riskier investments or unnecessary financial austerity in your productive years. By contrast, a realistic target tied to your actual needs lets you invest steadily, spend reasonably now, and retire with clarity. It also makes you to focus on your investment portfolio risk, something you can manage with tools like MyPlanIQ’s Fixed‑Income and Tactical Portfolios, which aim for low‑volatility, inflation‑beating performance for retirement savings. Individuals Vary Of course, the above is just a ‘typical’ American. For all of us, we are anything but an exact typical. For people who have higher income, you can easily see that your retirement savings needed for a comfortable retirement life can double or even triple (for a person with $180,000 annual compensation before retirement, for example). Of course for such a person with $180,000 before retirement, she or he indeed might need 3*600,000 or $1.8m savings! The point is, everyone should take time to run some numbers using the basic rule of thumb discussed in this article to understand their own situation. Headline figures are just headlines. They meant to grab your attention. But the real story is always in the details.

-

The Best Age (62, 67, or 70) to Claim Your Social Security Benefits

In this issue:

- Latest in Retirement Savings & Personal Finance: Social Security Benefit Tax in One Big Beautiful Bill, The Worst US Treasury Bond Returns in History!

- The Best Age (62, 67, or 70) to Claim Your Social Security Benefits

- Tools & Tips: Social Security Benefit Claim Age Calculator

- Market Overview

-

Retirement Withdrawals in Optimal Order

In this issue:

- Latest in Retirement Savings & Personal Finance: Amazon Prime Day Record Sales, Inflation Rise Again? Underestimating Hobby and Pastime Costs

- Retirement Withdrawals in Optimal Order

- Tools & Tips: Retirement Withdrawal Optimal Calculator

- Market Overview

-

Best Strategy to Withdraw Funds in Retirement

When you retire, the order you pull funds from your accounts (whether taxable, traditional, or Roth) can make big difference.

-

Retirement Milestone Cheat Sheet

In this issue:

- Latest in Retirement Savings & Personal Finance: OBBB Tax Changes, More Debt Among Millennials, Adult Children Living at Home

- Retirement Milestone Cheat Sheet

- Tools & Tips: Main ETFs You Can Use

- Market Overview

-

Savings Hacks

In this issue:

- Latest in Retirement Savings & Personal Finance: Crypto in 401(k), Private Investments in Target Date Funds, BNPL Credit Score Impact

- Savings Hacks Using BNPL & Others

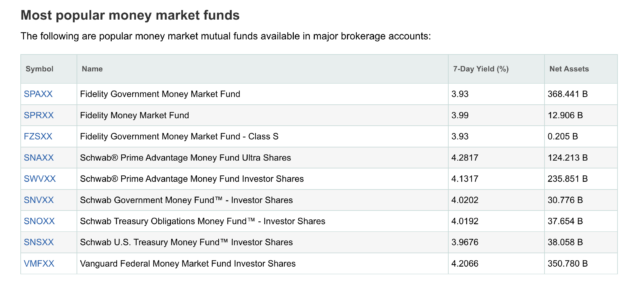

- Tools & Tips: Money Market Fund Center

- Market Overview

-

July 2025 MyPlanIQ Portfolio Update

In this issue:

- Residential Real Estate vs. Stock Investments

- Fund Analysis: PIMCO Multisector Bond ETF PYLD

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

Annuity Income Payout vs. Invest & Withdraw

In this issue:

- Latest in Retirement Savings & Personal Finance: Annuity Is Back, HSA & Retirement Healthcare Improvement, Growing Medical Debt Crisis

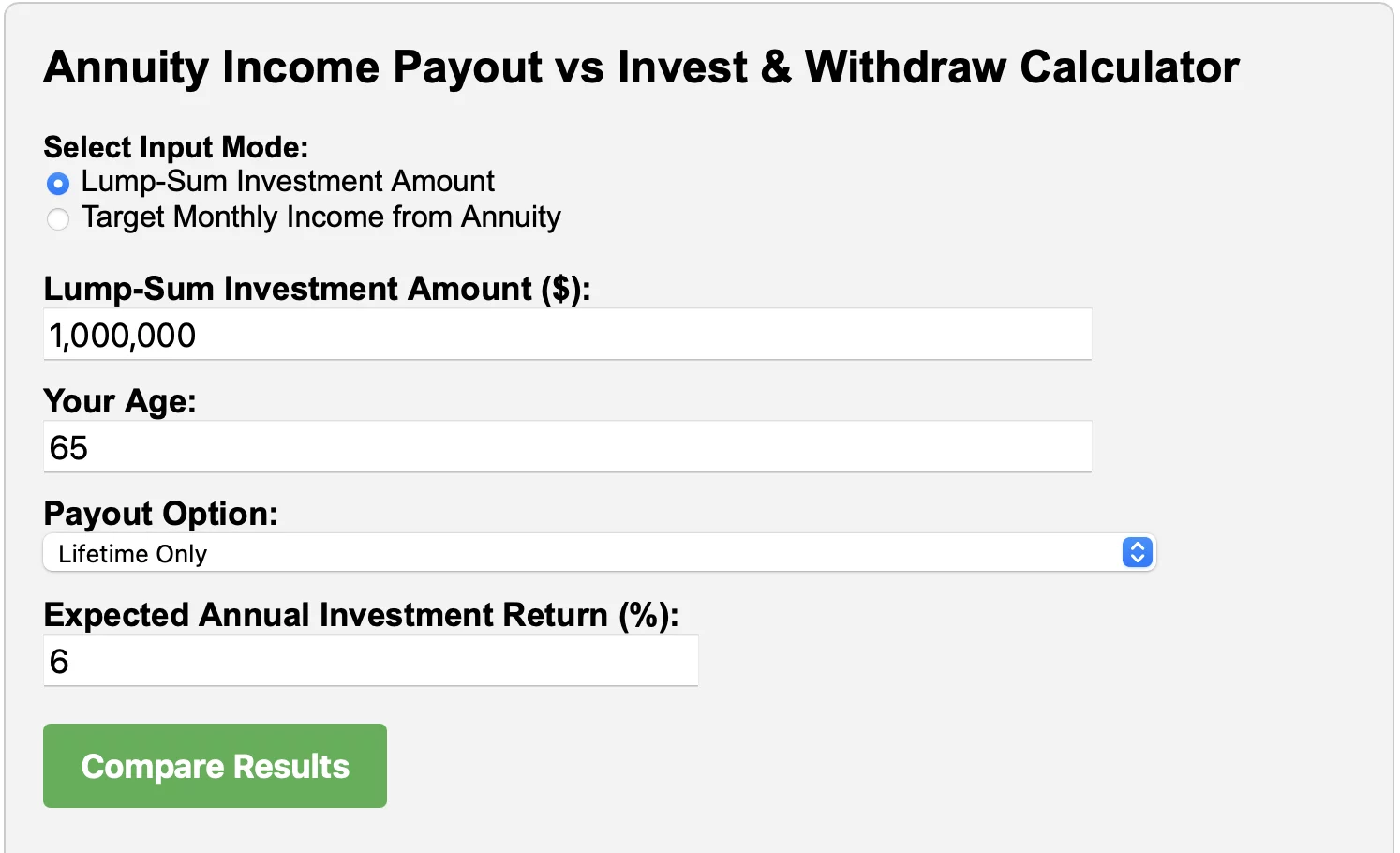

- Tools & Tips: Annuity vs Invest Calculator

- Annuity Income Payout vs. Invest & Withdraw

- Market Overview

-

What $1 Million Really Buys You in Retirement: Annuity vs. Investment Strategy

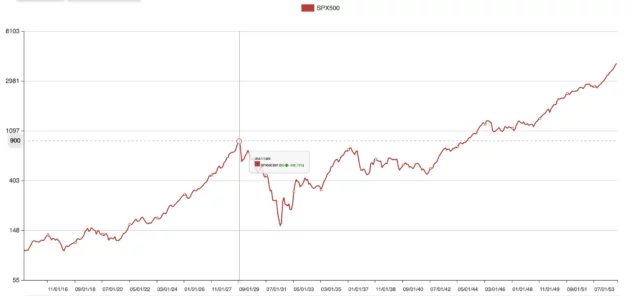

Most investors think about returns first. But what gets less attention, and probably deserves more, is volatility. Risk adjusted returns matter more. Being comfortable with portfoiio swings is the key to investment success.

-

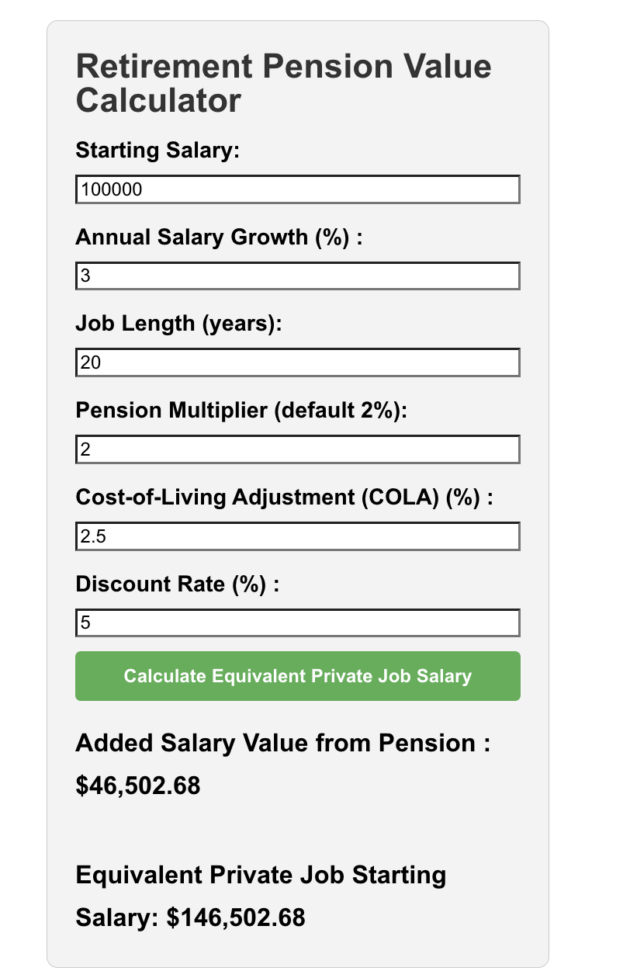

Public Pay Might Be Higher Than You Think (Once You Do the Math)

In this issue:

- Latest in Retirement Savings & Personal Finance: High 401(k) Savings Rate, The Big Beautiful Bill’s Deficit Increase & Who Are Affected by the BBB

- Public Pay Might Be Higher Than You Think (Once You Do the Math)

- Tools & Tips: Retirement Pension Value Calculator

- Market Overview

-

Why Managing Volatility Matters

Most investors think about returns first. But what gets less attention, and probably deserves more, is volatility. Risk adjusted returns matter more. Being comfortable with portfoiio swings is the key to investment success.

-

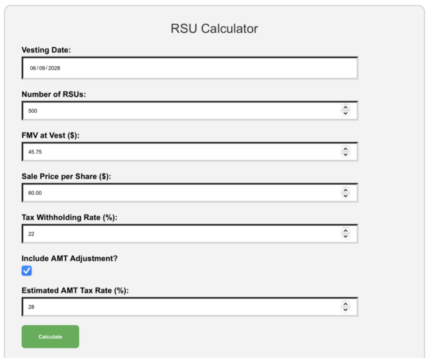

Stock Compensation 101: How People Build Wealth (or Blow It)

In this issue:

- Latest in Retirement Savings & Personal Finance: Review and Get Rid of Your Unused Subscriptions, Private Equity & Crypto Investments in Your Retirement Accounts, Germany’s Early Start Pension

- Stock Compensation 101: How People Build Wealth (or Blow It)

- Tools & Tips: RSU Calculator

- Market Overview

-

Retirement Plan Contribution Limits in 2024

2024 Retirement Plan Contribution Limits 1. 401(k), 403(b), and 457(b) Plans Employee Contributions: Up to $23,000 (under age 50) Catch-up contribution: $7,500 (ages 50+) Total Combined Limit (Employee + Employer): $69,000 Roth Options: Available for 401(k), sometimes for 403(b) and 457(b) Plan Details: 401(k): Primarily for for-profit companies; includes Roth (after-tax) options. 403(b): For public schools and nonprofits; Roth-style options less common. 457(b): For state/local government and some tax-exempt organizations; Roth availability varies. 2. Solo 401(k) and SEP IRA Solo 401(k): For self-employed individuals/business owners without employees.

- Employee contributions: $23,000, plus $7,500 catch-up (ages 50+)

- Employer contributions: up to 25% of compensation

- Total combined limit: $69,000 or 25% of compensation, whichever is less

SEP IRA: Employer contributes up to 25% of compensation, up to $69,000. No catch-up contribution. 3. SIMPLE IRA

- Employee contribution: up to $16,500

- Catch-up contribution: $3,500 (50+)

- Employer must match dollar-for-dollar up to 3% of employee salary

- Immediate vesting

4. Traditional and Roth IRAs

- Annual contribution: $7,000

- Catch-up: additional $1,000 (50+)

Traditional IRA: Pre-tax contributions, taxable upon withdrawal Roth IRA: After-tax contributions, tax-free withdrawals 5. Thrift Savings Plan (TSP)

- Federal and uniformed services employees only

- Employee contributions: up to $23,000 (under age 50), plus catch-ups ($7,500 at 50+)

- Employer matches up to 5% of salary

- Total Combined Limit (Employee + Employer): $69,000

- Pre-tax (traditional) and Roth contributions allowed

6. Payroll Deduction IRA

- Annual limit: $7,000; catch-up of $1,000 (age 50+)

- Pre-tax or Roth contributions

- No employer matching

7. Health Savings Account (HSA)

- Individual coverage: $4,150

- Family coverage: $8,300

- Catch-up contribution: additional $1,000 for age 55+

- Must have a high-deductible health plan

- Tax-free growth; penalty-free medical withdrawals; penalty-free non-medical withdrawals after age 65 (taxable)

8. Self-Directed IRA (SDIRA)

- Contribution limits same as IRAs ($7,000 + $1,000 catch-up age 50+)

- Allows alternative investments (real estate, precious metals, crypto)

- Requires IRS-approved custodian

9. Nondeductible IRA

- Same limits as traditional IRAs ($7,000 + $1,000 catch-up age 50+)

- Contributions not tax-deductible; earnings taxable at withdrawal

10. Annuities and Pension Plans (Brief Overview)

- Annuities: Insurance-based retirement products, providing guaranteed income. High fees, limited liquidity.

- Pension Plans: Employer-funded defined-benefit plans providing guaranteed lifetime income. Limited investment control.

11. Flexible Spending Account (FSA) Limits for 2024

- The maximum employee contribution to a health care FSA for 2024 is $3,200.

- If the FSA plan allows for carryover, the maximum amount that can be carried over to 2025 is $640.

- For Dependent Care FSAs, the maximum remains $5,000 per household (single or married filing jointly) or $2,500 if married and filing separately.

12. Health Savings Account (HSA) Limits for 2024 Coverage Type 2024 Contribution Limit Catch-Up (Age 55+) Minimum Deductible Out-of-Pocket Max Self-only $4,150 +$1,000 $1,600 $8,050 Family $8,300 +$1,000 (per eligible spouse, each in own HSA) $3,200 $16,100

- Individuals age 55 or older can contribute an additional $1,000 as a catch-up contribution.

- HSA contributions can be made until the tax filing deadline (April 15, 2025, for tax year 2024).

- To be eligible for HSA contributions, you must be enrolled in a high-deductible health plan (HDHP) meeting the minimum deductible and out-of-pocket maximum requirements above.

-

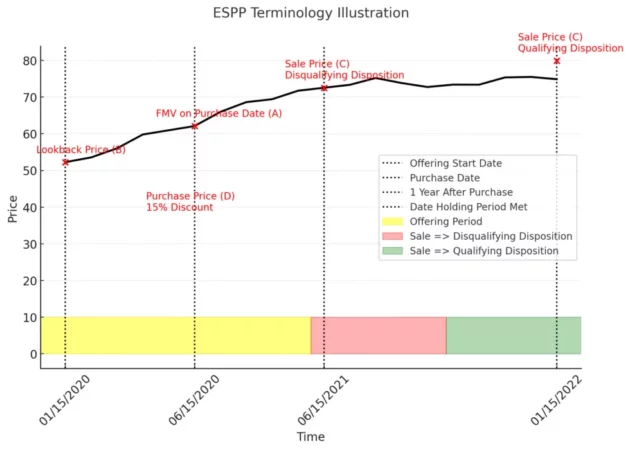

How to Take Advantage of Your ESPP (Employer Stock Purchase Plan)

In this issue:

- Latest in Retirement Savings & Personal Finance: Workplace Benefits like Flexible Spending & Telemedicine, AI Taking over Jobs?

- How to Take Advantage of Your ESPP (Employer Stock Purchase Plan)

- Tools & Tips: ESPP Tax and Cost Basis Calculator

- Market Overview

-

June 2025 MyPlanIQ Portfolio Update

In this issue:

- MyPlanIQ Composite Allocation Indicator & Applications

- Fund Analysis: Factor Funds & Healthcare Industry Trend

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

How to Benefit from Your ESPP (Employer Stock Purchase Plan)

This article explains how to benefit from your ESPP (Employer Stock Purchase Plan) by looking at both short and long terms.

-

Simple 401(k) Investment Guide

In this issue:

- Latest in Retirement Savings & Personal Finance: College Education Affordability Declined, Rising Debt Puts Your 401(k) Retirement Savings in a Pickle

- Simple 401(k) Investment Guide

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

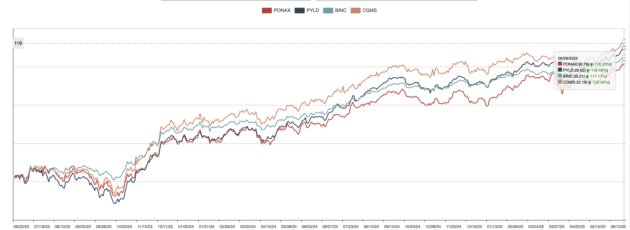

Why Actively Managed Bond Funds Outperform Index Funds More Often Than Stocks

Multiple research results now point to what seems like a consistent pattern: active bond funds tend to outperform their passive peers more often than stock funds do.